Multifamily renter demand in the U.S. has quietly reached a historic milestone.

In 2025, the number of multifamily rental households climbed to 22.4 million, the highest level ever recorded, according to research from Chandan Economics and Arbor Realty Trust.

This isn’t a short-term spike or a post-pandemic anomaly. It’s the continuation of a multi-year structural shift that is reshaping the housing landscape—and creating long-term implications for investors focused on durable income and demand-backed assets.

A Growth Trend with Staying Power

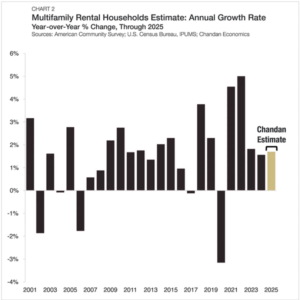

Multifamily household formation has now grown at a steady 1.6%–1.8% annual rate for three consecutive years. From 2020 to 2025, the sector expanded by 15.4%, dramatically outpacing the 5.3% growth in total U.S. households over the same period.

In absolute terms, the U.S. added nearly 3 million multifamily households over the past five years, the largest net gain since 2000.

For investors, the significance lies less in the headline number and more in the consistency. This level of growth suggests not a cyclical surge, but a durable rebalancing of where and how Americans choose, or are forced, to live.

Supply Has Risen—but So Has Absorption

Importantly, this demand growth has occurred alongside a historic wave of new supply. In 2024 alone, developers delivered 591,400 multifamily units, the highest annual total since 1974. Through August 2025, another 328,500 units came online, keeping completions elevated.

Rather than overwhelming the market, this supply surge has largely been absorbed.

Without it, household growth within multifamily would have been constrained, placing even greater pressure on rents and occupancy. Instead, new deliveries helped accommodate record demand while preventing excessive overheating in many markets.

This balance between supply and demand has been a key factor in the sector’s resilience.

Structural Demand Drivers Remain Intact

Several long-term forces continue to support multifamily growth.

The cost of homeownership has moved further out of reach, with mortgage payments, insurance, and taxes consuming approximately 43% of median household income, well above traditional affordability thresholds. At the same time, return-to-office policies have reinforced demand in employment-dense metros, particularly among renters seeking proximity and flexibility.

In certain Sun Belt markets, rising numbers of high-income renters are adding competitive pressure to the rental pool, further reinforcing demand even as new supply delivers.

Together, these forces suggest that multifamily demand is not solely a function of interest rates or short-term economic conditions, but a reflection of broader affordability and lifestyle realities.

What This Means For Investors in 2026

Despite record household counts and elevated deliveries, occupancy has remained relatively stable, and rent pressure has moderated rather than collapsed. This points to a market that is absorbing growth, not struggling under it.

As construction pipelines begin to normalize and demand drivers remain structurally intact, the multifamily sector is expected to enter 2026 on more balanced footing, characterized by steadier household growth, stabilized rents, and improved visibility for long-term investors.

For accredited investors, this matters because durable demand is the foundation of every successful multifamily strategy. Record household formation doesn’t guarantee outsized returns on its own, but it does create a strong base for disciplined operators, selective market exposure, and strategies focused on sustainability rather than speculation.

In a housing market defined by affordability constraints and evolving lifestyle preferences, multifamily’s growth story appears less cyclical and more structural, and increasingly difficult to ignore.

When You’re Ready… Here’s 3 Ways We Can Help:

- Connect With Our Team: Whether you’re exploring passive real estate for the first time or you’re a seasoned investor looking for a trusted partner, our team is available to answer your questions. Schedule a confidential strategy call to learn more about our investment philosophy, current opportunities, and how we help investors achieve income, growth, and tax efficiency.

- Join Our Private Investor Portal: Gain exclusive access to our current offerings and ongoing pipeline of multifamily investments. Inside, you’ll find detailed financials, market insights, and structured deal overviews—all designed to help you make informed, confident decisions about where to place your capital.

- Review Our Investment Strategy: Get a clear understanding of how we source, underwrite, and manage multifamily assets. Our strategy is built around long-term wealth creation, consistent passive income, and disciplined risk management. Learn what sets us apart and why sophisticated investors choose to partner with us.