The mood surrounding the multifamily investment strategy is shifting. Investors, lenders, and operators have signaled renewed confidence in the sector. After a cautious 2025, improving capital access, institutional re-engagement, and potential distressed asset sales suggest the early stages of a healthier transaction environment.

For investors, the question is no longer whether opportunities will emerge, but where to position capital as the cycle turns.

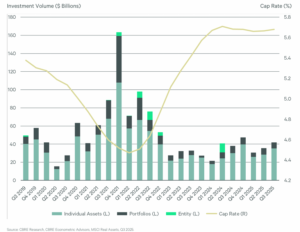

Institutional Capital Is Re-Entering the Market

Insights reported by Marcus & Millichap indicate that investors are widening acquisition criteria and preparing for increased deal activity in 2026.

What this means for you:

- Institutional buyers plan to increase transaction volume, signaling growing confidence in multifamily fundamentals.

- Acquisition criteria are expanding, creating liquidity across a broader range of assets and markets.

- Fewer syndicators are participating, but those active tend to be experienced operators with proven performance.

This environment favors investors aligned with strong operators and disciplined execution rather than speculative strategies.

Supply and Job Growth Will Shape Market Performance

While optimism is returning, structural pressures remain.

Headwinds to monitor:

- Elevated supply levels in many Sun Belt markets

- Slower job growth in certain regions

- Lease-up pressure for recently delivered properties

Markets with heavy new deliveries may experience temporary softness in rent growth and occupancy. Investors should prioritize submarkets with durable demand drivers and limited future supply pipelines.

Debt Capital Is Becoming More Accessible

One of the most meaningful shifts for investors is improved financing availability.

Agency lenders such as Fannie Mae and Freddie Mac have increased multifamily lending allocations by approximately 20%, while private lenders are re-entering the space.

Why this matters to you:

- Improved liquidity supports acquisitions and refinancings.

Expanded debt availability increases transaction velocity.

Financing terms may gradually improve if interest rates ease modestly.

However, rate volatility remains a factor, making conservative underwriting essential.

Distressed Loan Resolution May Create Buying Opportunities

Lenders are shifting their approach to troubled loans. Rather than repeatedly extending maturities, banks are increasingly bringing distressed assets to market.

Investor implications:

- Pricing discovery may accelerate.

- Discounted acquisitions could become more available.

- Market clarity improves as problem assets are resolved.

For investors with liquidity and patience, this environment may present rare opportunities to acquire assets at favorable bases.

How to Position Yourself in 2026

Here are several trends should inform investor decision-making:

Capital is returning.

Institutional activity suggests strengthening conviction in multifamily as a core asset class.

Financing conditions are improving.

Greater debt availability enhances your ability to transact and refinance.

Distress may create entry points.

Loan resolutions could unlock below-replacement-cost opportunities.

Market performance will diverge.

Supply-heavy metros may underperform while constrained markets maintain pricing power.

Selectivity remains critical.

Employment growth, migration patterns, and supply pipelines will determine asset performance.

The Bottom Line for Investors

Multifamily is entering 2026 with renewed momentum, but not without complexity. For investors refining their multifamily investment strategy, the current environment demands both patience and precision. Improved debt access, institutional re-engagement, and potential distressed sales point toward a stabilizing investment environment. At the same time, supply pressures and uneven economic growth reinforce the need for disciplined market selection and operator strength.

For investors, this phase of the cycle rewards preparation and strategic positioning. The opportunities emerging now are unlikely to be driven by rapid appreciation, but by acquiring quality assets at favorable bases, securing durable financing, and aligning with experienced operators.

Those who position capital thoughtfully today will be best prepared to benefit as the recovery matures.

When You’re Ready… Here’s 3 Ways We Can Help:

- Connect With Our Team: Whether you’re exploring passive real estate for the first time or you’re a seasoned investor looking for a trusted partner, our team is available to answer your questions. Schedule a confidential strategy call to learn more about our investment philosophy, current opportunities, and how we help investors achieve income, growth, and tax efficiency.

- Join Our Private Investor Portal: Gain exclusive access to our current offerings and ongoing pipeline of multifamily investments. Inside, you’ll find detailed financials, market insights, and structured deal overviews—all designed to help you make informed, confident decisions about where to place your capital.

- Review Our Investment Strategy: Get a clear understanding of how we source, underwrite, and manage multifamily assets. Our strategy is built around long-term wealth creation, consistent passive income, and disciplined risk management. Learn what sets us apart and why sophisticated investors choose to partner with us.